Less Stubborn

China’s leaders appear to be back on a pragmatic macro policy path, but more course corrections will be required to change the direction of the world’s second-largest economy. Beijing must continue to be less stubborn, and we will need to be patient.

In the August Sinology, titled “Stubborn,” I wrote that “Xi Jinping refused to acknowledge and fix problems which are preventing the Chinese economy from returning to a stronger growth rate.”

I described this as frustrating but said that “I believe that at some point, Xi will accept that to achieve his economic goals he must take steps to restore confidence among the country’s entrepreneurs and consumers.”

The August Sinology provided four reasons why I’m stubbornly convinced that Xi will eventually overcome his stubbornness and make the changes necessary to put China back on track to reach its potential growth rate:

- First, Xi presumably understands that entrepreneurs and consumers are the engine of China’s economic growth and that he must act to restore their confidence.

- Second, since last year, Xi has promoted an economic strategy focused on innovation which depends on entrepreneurs. Success in industries such as batteries and artificial intelligence (AI) requires a more supportive approach to the private sector.

- Third, Xi must recognize that failing to overcome his stubbornness to address the concerns of entrepreneurs and consumers may have negative consequences for social stability.

- Fourth, recently published second quarter macro data shows a clear deceleration in the pace of economic activity which should incentivize Xi to overcome his stubbornness and course correct.

Given the recent changes to monetary policy and measures to support the property market, can we conclude that Xi has stopped being stubborn?

In my view, while Xi hasn’t yet fully abandoned his stubbornness, he is clearly on the path towards doing so. It is important that he has acknowledged the seriousness of the steady decline in economic activity, especially in real estate. But he has yet to do enough to even stabilize the economy.

The good news is that Xi’s thinking seems to be moving in the right direction, and he is likely to soon fully overcome his stubbornness and deliver the rhetoric and policies that will rebuild trust among China’s entrepreneurs and consumers. The Fed’s recent rate cut also gives Xi more room to further relax monetary policy. We do not, however, know how long it will take for this process to fully play out.

And remember that when Xi does finally course correct in a pragmatic way, it is likely that Chinese entrepreneurs and consumers will bounce back. They have, historically, been tremendously resilient.

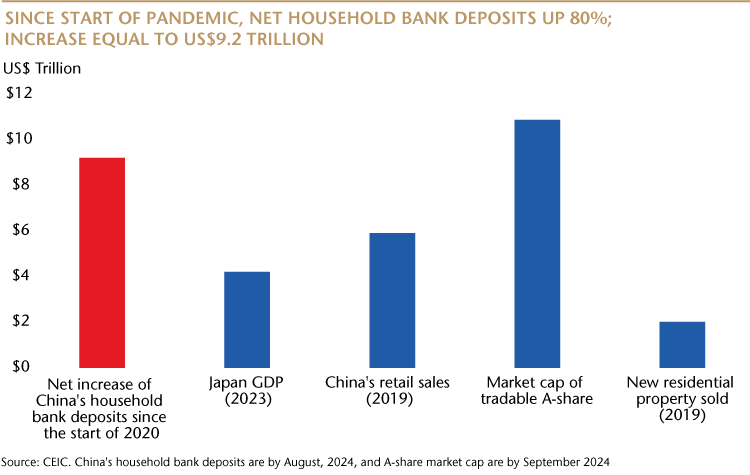

That resilience is likely to be supported by continued accommodative monetary policy and high savings. Family bank balances have increased 80% from the start of 2020, as Chinese households were in savings mode during the country’s zero-COVID policy. The net increase in household bank accounts is equal to US$9.2 trillion, which is greater than the GDP of Japan in 2023, and greater than the value of China’s pre-COVID 2019 retail sales. In my view, this could be significant fuel for a consumer spending rebound, as well as a sustainable recovery in mainland equities, where domestic investors hold about 95% of the market.

Andy Rothman